So, you’re thinking about buying your first home?

If you’ve asked, and already answered the question: “Is it better to rent or own?”

And decided that you’re ready to buy a home... You did your research, looked at your local real estate market and compared the costs of renting vs owning for you and your situation...

And now you just need to decide: "As a first time home buyer, should I buy a condo or a single family house?"

What We Know About Buying A Condo As Realtors & Real Estate Experts

With 20 years of experience in real estate, I don't just rely on my expertise and old school tactics. I've embraced digital media as a way to share withs possible with real estate with buyers and sellers.

I rank for searches on YouTube like "buying a condo." Even a head of Financial Expert, Best Selling Author and Radio Personality Dave Ramsey.

... and "home buying tips" in front of Million Dollar Listing New York, Ryan Serhant. And Realtor.com's spokesperson and celebrity, Elizabeth Banks.

Katherine and I decided that it was time to take what we have shared in video and podcasts and put in "print," so to speak. And that's exactly what you'll get in this step-by-step deep dive on buying a condo.

What We Know About Buying A Condo As A First Time Home Buyer

I was 19, on a trip visiting my brother in Utah. He had just become a real estate agent.

I had just graduated from high school a year or two before.

I’m not sure I was quite over the initial disappointment that I didn’t go to college, like the rest of my friends.

I was thinking to myself I should come to terms with the fact that I’d never be really successful. Because of the attitude I had, I thought I should probably work as much and as hard as possible while I:

- Didn’t have any friends around anymore because they had all gone off to college and

- Might as well fill my time with work and save some money so that I could travel, buy a car, move out of my parents’ house, go to to school, or something else.

My Plan:

Step 1: Save money.

Step 2: Figure out what to do with it later.

Even though I didn’t have the most positive, confident outlook on life and money at the time, I started to understand the concept that money opens doors.

Back to my Utah trip: My brother took me to his real estate brokerage office to show me where he worked. While I was there, I was hanging out in his office while he talked to one of his colleagues. I picked up a book off his shelf called “The Automatic Millionaire Homeowner,” by David Bach.

I “borrowed” the book from his office and ended up reading the entire book on the plane ride home, back to Seattle.

I was drawn to the content in the book. Probably because it was one of the first times in my life I was told that wealth doesn’t have to start with good grades and a college degree.

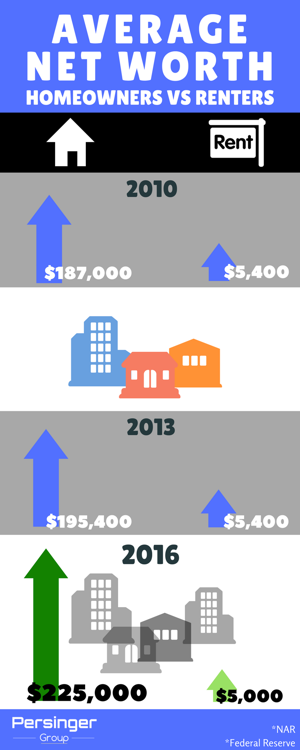

In one of the first pages of the book, I read that: The average net worth of a renter is $5000. The average net worth of a homeowner is $175,000.

***Note, today, in 2017, the average net worth of a renter is $5000, and the average net worth of a homeowner is $225,000.

***Note, today, in 2017, the average net worth of a renter is $5000, and the average net worth of a homeowner is $225,000.

You’ll notice the renter’s net worth hasn’t changed since 2005 (when the book was written). Absolutely no offense to renters. Everyone has their reasons, and their priorities. But I knew when I heard that stat which group I wanted to be a part of.

I was living with my parents at the time. It occurred to me that since you have to live somewhere, you might as well be getting ahead by owning a home, rather than getting behind, or maybe staying put, while renting.

Since becoming a real estate agent in late 2008, and buying my condo in 2009, I live and breathe this statistic.

My Personal Condo Buying Experience

Back on November 14th, 2008, I knew I wanted to buy a home, but didn’t know for sure where.

I was literally looking everywhere in between Issaquah and Marysville.

Yes, that is a LOT of ground to cover. I put a lot of thought into it… And decided Mukilteo, WA would be a good move because of the proximity to freeways, the beach, the ferry, and Puget Sound.

I picked the beautiful and desirable Harbour Pointe neighborhood, which is great for walks in the summer, nice and close to restaurants, grocery stores, banks, doctors/dentists, and more.

But it wasn’t that simple.

I wrote an offer for my dream condo. It got accepted, and I was on cloud nine.

After a couple weeks, I got a call from my lender who was kind of a robot, and didn’t know how to break this gently to me. “Katherine, you’re not going to qualify. Your ratios are all out of whack.” (or something like that).

Maybe this wouldn’t be a big deal to everyone. But I was barely even licensed as a real estate broker and I had never been through a transaction before. I didn’t know what this home buying process was like.

It hit me like a ton of bricks.

To add to this… the phone call was as I was on my way into meet my brother’s new girlfriend (they’re married now). It was a pretty awkward first meeting… I was holding back tears.

I hated everyone and everything in sight.

We’re okay now, and I think she’s forgiven me for being a little stand-offish! But guess what? It wasn’t the end of the world.

I didn’t end up buying that condo unit, but I found a slightly smaller and less expensive condo in the same building. I was happy in it and still have it as an investment property.

It was a great first home purchase, and in hindsight, I wouldn’t have it any other way. I knew I wanted to buy because I wanted my payments to go toward my equity. I wanted to be able to paint my walls, switch out light fixtures, and overall, make it my own.

I love the idea of one day having my condo paid off, earning rental income, and getting a tax write-off while I’m at it. I love real estate… I love owning it.

Maybe you decided that being a homeowner is for you because it gives you a path to wealth.

Warren Buffett thinks real estate is a good buy because of the 30-year mortgage. "A 30-year mortgage is the best instrument in the world. Because if you're wrong and rates go to 2 percent, which I don't think they will, you pay it off. It's a one-way renegotiation. It is an incredibly attractive instrument for the homeowner and you've got a one-way bet." - Warren Buffett

Maybe you decided to buy a home because you want the stability, don't want to be at the mercy of landlord telling you what you can, can't do and surprise rent hikes.

We're sure you've looked at the pros and cons, so this guide is not about trying to convince you why buying a condo is good idea, or why you should continue renting.

This Ultimate Guide For First Time Home Buyers looking at buying a condo is going to show you everything you need to know about being condo buyer as buying your first home.

Introducing: The Ultimate Guide For First Time Home Buyers Buying A Condo

Here is how you get started.

When you click one of the chapter links below, it will jump you to your desired chapter… without refreshing the page.

So, pick which chapter you like and get started.

- Chapter 1: Condo vs Townhome vs Coop: What's The Difference

- Chapter 2: Condo vs Single Family - 5 Reasons Why Buying A Condo Is A Smart Alternative For The First Time Homebuyer

- Chapter 3: Condo Mortgages Getting Your Personal Finances In Order

- Chapter 4: How To Find Your Condo: Online Search vs Open House vs Private Tours

- Chapter 5: How To Make An Offer On A Condo You Want To Buy

- Chapter 5.5: WAIT

- Chapter 6: It Just Got Real. Congrats!!!

- Chapter 7: What To Expect As You Get Ready To Close On Your Condo

- Chapter 8: Frequently Asked Questions About Buying A Condo (Questions You Should Ask)

Condo vs Townhome vs Coop

CHAPTER 1

5 Reasons Why Buying A Condo Is A Smart Move

CHAPTER 2

Condo Mortgages

CHAPTER 3

How To Find Your Condo

CHAPTER 4

Making An Offer On A Condo

CHAPTER 5

WAIT

CHAPTER 5.5

.png)

It Just Got Real

CHAPTER 6

Ready To Close On YOUR Condo

CHAPTER 7

Buying A Condo FAQ's

CHAPTER 8

Chapter 1: Condo vs Townhome vs Coop: What's The Difference

In this chapter you'll get answers to questions like,

- What's a condo?

- What's a townhome?

- What's a co-op?

- What's the difference between a condo vs townhome vs coop?

And you'll get some additional info about types of real estate you might not even know of.

When people start talking about a condo and how it's different from a house you get simplified answers and definitions, like, "A condo is like an apartment but you own it," or "a condo is like a home without a yard."

So starting off we'll give you some definitions of what these different types of real estate and ownership are.

This will be based on the state of Washington, since that's where we sell real estate. And then we'll give you some additional links for more info on condos, townhomes, and co-ops.

What Is A Condo (Condominium)?

A condominium unit is created by a Washington state statute (RCW 64.34) which involves a survey to locate each unit as a “parcel” of land. Meaning not only the four walls, but the floor and ceiling.

Basically a condo is "box" at a specific location, because you don't own above you or below you. You own everything within this box.

And you'll also have ownership in a percentage of the common area or common elements – everything outside the box. The grounds, parking lot, common buildings (such as a pool, weight room, lobby) elevators, and hallways are the commons.

EXAMPLE: Courtney buys a condo unit in a 48-unit condominium community. The deed describes her property as "Unit 21 in Sherwood Point, a condominium, together with an undivided 1/48 interest in the common areas of said condominium."

FUN FACT ABOUT CONDOS: Condos are not only residential. Condos can also be office space, retail or even storage units.

What Is A Townhome?

A townhome mixes parts of condos and single family housing. A townhome is typically a mulit-story home on a small lot. It may or may not have shared walls with other property. Townhome ownership is similar to owning a condo in that you have both ownership in your unit and co-ownership in the common areas. The major difference of a townhome vs a condo though is that a townhome owner has title to the parcel of land on which the townhome sits.

Other types of ownership:

Coops (Cooperatives)

In a coop, you don't actually own real estate. You own stock in a corporation that owns the real estate. Coops are more popular in some areas than others. There are a few residential coops in the Seattle area, (check out a list of cooperative residences in Seattle from Seattle Wiki) but many more in the New York area.

A good place to start on finding a co-op is at National Association of Housing Cooperatives.

FUN FACT: In Manhattan, it’s about 75 percent co-op versus 25 percent condo.

- Co-Op vs. Condo: What You Need to Know | Huffington Post

- What Is a Co-op? A Home You Don't Technically Own | Realtor.com

- Towndo Phenomenon - Condos Vs Townhouses | Good Life Team

- Condo vs. Townhouse - What's the Difference? | Byers Team

Chapter 2: Condo vs Single Family - 5 Reasons Why Buying A Condo Is A Smart Alternative For The First Time Home Buyer

Let's talk about a condo as an alternative to buying a single family home for your first home purchase.

As I mentioned earlier, so many people think of a single family home as the home purchase.

Many people don't think about a condo, or possibly a townhome, as a potential purchase, or if maybe they've thought about it and completely dismissed it without really looking into it. Home buyers have a romantic idea that their first home purchase has to have a front yard, a back yard, a white picket fence, a place where the kids and the dog can run around in the yard, and you can look out your window, and see all that going on.

That's a beautiful, wonderful, romantic idea, but it doesn't always work out that way. And it doesn't have to be that way.

You can get into your first real estate purchase by buying a condo.

Here are five reasons why you might want to look at a condo as your first home purchase.

Number 1: A condo has the benefit of lower maintenance.

Maybe you're busy because of your career, or your social life, or you're someone who likes to travel and you're going to be gone for a lot of weekends because you're doing this or that, or you're going to be gone for long extended periods of time because your work involves travel.

Mine did for a long time.

As a paid speaker, I was traveling around the country 30 to 40 times a year. It would have been very hard to maintain a yard, and do everything involved with upkeep, especially if I lived back in Wisconsin where during winters I would have been shoveling the sidewalks and the driveway.

Lower maintenance is a huge benefit of owning a condo, because it's built into your monthly condo association dues. Also the condo association dues, cover things like the outside maintenance of the condo, the roof, so you don't have to worry about setting money aside to take care of those maintenance issues that are going to come up with a single family house.

Your condo owners association is doing that for you with the monthly dues that you're paying. There is some value in what you're paying for those monthly condo dues.

Number 2: Condo Community

I've heard people complain about living in apartments, not really liking their neighbors.

Or not even knowing who their neighbors are because people are constantly coming and going. I can see the truth in that.

Apartment dwelling does not allow for a lot of community building.

I've lived in a few apartment communities before where I know the property management team is working really hard to build some community. They have community days, and things to do around the complex, but it's hard when people are so transient in that community.

One of the other benefits of condo/townhome living is you know those people are going to be there for a while. When people own their home they want to get to know their neighbors because if there's something going on, they want to be able to have an open communication dialog, or at least have a general respect for each other. "Because you own that place, and I own this place, and we own all of that together, let's have respect for each other." There's value in the just knowing who your neighbors are.

Number 3: The Condo Amenities

The amenities that you could potentially get with a condo or townhome community far exceed what you're going to get with a single family house.

Now there's always a cost for these amenities. There's a correlation to the cost and the amenities that you're going to get. The better the amenities, most likely, the higher you're going to be paying in your association dues.

There's a lot of potential when buying a condo to end up having a pool, a fitness room, a theater room, walking trails, tennis courts, basketball courts, all sorts of different things, that unless you're buying a single family home that is a mansion, you're not getting those things as part of your estate.

When you're buying into a condo community, and it's built into your association dues, there is fairly decent chance that you're going to end up with amenities like this. Or you can even focus only on buying a condo in the communities that have the amenities you want.

If having a pool, and a hot tub, and a fitness area, and things like that, are important to you, you can definitely find it out there in your condo search.

When you're buying a condo, there is a much better chance that you're going to get more interesting amenities than you would if you were buying a single family home.

Number 4: Investment With Benefits

I'm going to combine four and five here.

If I was to compare single family homes to condos, over time I'm probably going to see a higher appreciation rate on single family homes versus condos.

Condos are still going to appreciate but most likely not as much as a single family home.

Seattle Condo Appreciation vs Seattle Single Family Homes

While writing this guide we decided to dive into the appreciation numbers to test our assumptions on how much condos appreciate in value versus single family homes.

Looking at the Seattle real estate market and comparing condos to single family you actually will see condos have increased in value almost 18% this year, while single family homes have only gone up in value 10%.

In 2016 Seattle condos increased in value over 21% while single family homes went up about 15%.

So as you can see even though single family homes are more expensive, condos are increasing in value faster.

We found this to be pretty interesting so we wanted to look at another market to compare home values vs condo values there.

We looked at the Snohomish County real estate market.

These numbers match up more with our experience and assumptions. Looking at the Snohomish county real estate market and comparing condos to single family you actually will see condos have increased in value almost 5.5% this year, while single family homes have only gone up in value almost 10%.

In 2016 Snohomish County condos increased in value almost 13% while single family homes went up about 10%.

There is an investment benefit to being a condo owner versus just continuing to pay rent, where the only thing that's increasing when you're renting, is your rent.

You could have your rent continuing to increase, or buy a condo and have it appreciate, perhaps even more than a single family home.

Number 5: Location, Location, Location

Another benefit of buying a condo is that you might be able to get a bit better location.

If you're really committed to having that yard with the fence, and that whole ideal of a single family home lifestyle, you're probably going to have to look little bit further away from a downtown area, from where there's more interesting things to do, from your work, from the metro area. Wherever it is that you most likely work, or socialize in, or where the best entertainment stuff, the best restaurants, the best place to go for drinks, the best things to do, to go have fun.

A single family home is going to be further away from that for the same type of money of your condo, which I would connect to number five.

BONUS: You Get More

You get more for your money with a condo or a townhome. Now this isn't the case in every market and every area, but generally you're going to get a lower price per square foot when you're buying a condo verses a single family home.

When you combine all of those things of being able to get a little bit more for your money, a better location which includes now that you have appreciation instead of just paying out rent all the time, the sense of community, of actually knowing who your neighbors are. There's a little bit of stability there. Not having to worry so much about maintenance of your property impacting other parts of your lifestyle, of you being busy career driven, or liking to travel, and just being away from your home a little bit more often. Not working about the upkeep of the yard, or the maintenance of the outside, anything like that. Those are the benefits of looking at a condo.

If you've never thought about a condo before, but you thought about it for a split second and then you dismissed it, because you thought of it too much like apartment living and that's what you're trying to get away from. I encourage you to look at this guide and the idea of buying a condo from a fresh perspective. It might be a little bit similar to apartment living, but there's a lot of other benefits to having a condo be your first home purchase.

Chapter 3: Condo Mortgages Getting Your Personal Finances In Order

According to a recent survey by the National Association of Realtors only 2 percent of home buyers said buying a home for financial security was their primary reason. And maybe that’s good.

At Persinger Group we don’t believe a home should be looked at as an investment. A home is where memories are created and memories are shared.

With that being said, there is definitely some financial upside to being a homeowner versus renting.

In a New York Times article published at the end of 2014, “Homeownership and Wealth Creation,” they discuss the decline in homeownership to a 20-year low.

The number of owner-occupied homes has stayed basically the same but there has been an increase in renters by nearly 25 percent. That is probably a good answer for the question of why does the cost of renting continue to increase. It’s simple supply and demand.

Going back to that New York Times article, the question they try to answer about the future of homeownership is: Would more and longer rentals be a bad thing? Are the benefits of homeownership overrated?

The answer to the first question is yes; the answer to the second is no.

“Homeownership long has been central to Americans’ ability to amass wealth; even with the substantial decline in wealth after the housing bust, the net worth of homeowners over time has significantly outpaced that of renters, who tend as a group to accumulate little if any wealth. A recent study by researchers at the Joint Center for Housing Studies at Harvard University analyzed the reasons for these differing outcomes. Paramount among them is that homeownership requires potential buyers to save for a down payment, and forces them to continue to save by paying down a portion of the mortgage principal each month. Renting, in contrast, offers the potential for comparable wealth building only if renters invest an amount equal to a down payment plus any savings from renting. As a practical matter, most renters do not do that. Even in instances where renters have excess cash, saving a substantial amount is difficult without a near-term goal, like a down payment. It is also difficult to systematically invest each month in stocks, bonds or other assets without being compelled to do so. The analysis does not downplay the risks of homeownership or the devastation of the housing bust. But the lesson of that debacle is not for individuals to avoid homeownership or for policy makers to devalue its importance.”

Real estate and homeownership is still the greatest path to wealth creation and the largest contributor to increased net worth. So it seems, the more things change - the economy, technology, etc - the more things stay the same.

At least how to create wealth in United States.

Own real estate.

Don’t Be Afraid Of Your Financial Grade

If you’re still reading good...

Some people will have already become bored, or afraid of the things we're talking about, they will have stopped reading and gone back to dreaming.

Just looking at homes online, but never doing anything to make the realty dream a reality.

And money and finances is one of the biggest fears that keeps people dreaming instead of actually owning a piece of the American Dream.

LoanDepot.com did a survey in 2014 and reported that just over half (56%) of all people who want to own a home but don't own a home, say they're not pursuing it because they fear they won't qualify for a loan.

Fear.

Plain and simple fear.

Not a low credit score or lack of down payment.

Potential homebuyers are rejecting themselves instead of having a mortgage lender do it.

Elsewhere in that survey, they discovered: While 71 percent of all Americans who want to buy a home in the next two years will need financing, 89 percent haven't actually taken any steps to see if they could get a home loan. Specifically, three quarters (74%) of people who want to buy a home but fear they won't qualify for a mortgage admit they haven't taken any steps to qualify.

You have to take some steps.

You have to take some action.

And even though it might be uncomfortable to talk about it, it starts with money.

I know it’s more fun to look at big, beautiful pictures of homes online or swipe at properties on your mobile device like you’re playing with Tinder, but Finding the One, comes after you get your money straight.

And I promise you, it’s easy.

I guarantee you it’s easier than you’re making it out to be in your head.

The Difference between Mortgage Pre-qualification and Pre-approval

Mortgage Pre-qualification is simply a rough estimate of how much you can borrow.

Pre-approval involves a formal application process and provides you with a formal commitment from a lender stating how much you can borrow and at what interest rate.

I know there are different mortgage calculators and apps out there and again, it’s fun to play with the numbers to try to figure out what you can afford, but to make home buying easy all you have to do is make a call to a local mortgage lender.

Yes. I said make a call.

Don’t try to email it in or waste more time going to a big bank website or to a national mortgage company that you see advertising on TV.

Keep it simple and call the bank or credit union you bank at.

Ask the real estate agent that you’re working with. If you’re wondering if you can trust the agent you’re working with to give you a fair recommendation, maybe they're getting a kickback or something, realize that they’d have to disclose that and you should ask anyway just to see how they respond to the question.

What you’ll find is if you have a relationship with your local mortgage lender you are more likely to get timely responses, answers and service. I like being able to walk into a local mortgage lender’s office and ask why hasn’t the appraisal been ordered yet.

When working with a big national company that’d you’d see on TV, I have to wait in a call queue, give a file or reference number and hope I don’t get transferred to someone else.

Experience shows that the local lender is going to work harder at not only keeping you happy, but your real estate agent happy.

The real estate world is small and if a lender screws a deal up, not only is an agent going to explain their hesitancy of a buyer working with that lender, but the agent will most likely tell her other agent friends.

The mortgage lending phone center people don’t care about their reputation at a local level. That makes me feel like they don’t really care about the deal as much also.

Getting Pre-Qualified For Your Mortgage

When you call the mortgage lender for a pre-qualification they are going to ask some simple, straightforward, questions.

They’ll want to know your employment history, your income, your monthly debt, any assets, how much you think you are going to put down and they might run your credit.

It’s really that easy.

Now, this doesn’t mean they are promising you that you can get a mortgage and there is no guarantee that you can actually afford what the number you come up with. But it gives you a great start while you start to get everything in order for a pre approval.

Knowing Your DTI (Debt to Income Ratio)

A debt-to-income ratio is a rule of thumb way for one lenders to measure your ability to handle the monthly mortgage payments along with your current debt burden. To calculate your DTI ratio, add up all your monthly debt payments and divide them by your gross monthly income.

Your gross monthly income is the amount of money you have earned before your taxes and other deductions are taken out.

Persinger Principle: A mortgage lender will tell you what you can afford, but you decide what will spend

So you can see how monthly debt can have an impact on how much of a monthly mortgage payment you can afford.

FOR EXAMPLE:

Let’s say Courtney and Christopher both make $5,000 a month.

However, Courtney has a $400 a month car payment, $300 a month in student loans and owes a minimum of $150 on her credit cards every month.

Christopher has a $300 a month car payment and has no student loans or credit card debt.

Courtney has a 17% Debt to income ratio before adding a mortgage payment.

If a mortgage lender is willing to loan her on a 43% DTI Ratio, she could get a $1,300 a month mortgage.

Looking at Christopher’s numbers now, only having a $300 a monthly car payment, he could qualify for monthly mortgage payment of $1,850 and stay in the 43% DTI Ratio.

You can run a hundred different examples, play with mortgage calculators online and try to figure out yourself but nothing will trump getting it straight from the horse’s mouth.

Schedule a time to call that mortgage lender right now.

Getting Pre-approved

Once you’ve called a mortgage lender to get pre qualified the next step would be to start to get everything together to get pre-approved.

Your lender will probably give you a list of what they specifically need, but here’s an idea to get you started:

CHECKLIST FOR GETTING PRE-APPROVED FOR A MORTGAGE

- Picture ID

- Social Security Number

- Complete addresses of all places lived (past 2 years)

- Employment history, including names, addresses, phone numbers, and length of time with that company (past 2 years).

- Copies of your most recent pay stubs and W-2 form (past 2 years).

- Verification of other income (social security, child support, retirement).

- Copies of all bank statements from checking/savings accounts (past three to six months).

- Copies of all stock/bond certificates and/or past statements/retirement accounts.

- Copies of title documents for all automobiles, boats, or motorcycles.

- Face amount, monthly premiums, and cash values of all life insurance policies

- Credit cards (account numbers, current balances, and monthly payments).

- Installment loans (car, student, etc.)

If you are self-employed:

- Copies of signed tax returns including all schedules (past 2 years), and a signed profit and loss statement for the current year.

Possible Other Info:

- Bankruptcy – bring discharge and schedule of creditors.

- Adverse credit – bring letters of explanation.

- Divorce – bring your Divorce Decrees, property settlements, quitclaim deeds, modifications, etc.

- VA only – bring Form DD214 and Certificate of Eligibility.

As I said, the list might be more than your lender requires or they might ask for more.

And don’t be surprised if they want updated information later on during the process. They might want to see new, updated bank statements, etc.

It might be frustrating or annoying to keep them updated with paperwork, but it’s easy if you stay organized.

Don’t Just Worry About Saving For The Down Payment

As you’ve made a commitment to become a homeowner, you’ve most likely already started saving for a down payment.

Now keeping in mind that not every buyer is going to have down payment and you might qualify for a zero down program, like a USDA or VA, or any new program that pops up, created by your lender or available to your local area, it’s still a good idea to start building up a nest egg.

Just because you can buy a property with zero downpayment doesn’t mean you shouldn’t be saving.

In fact, there are going to be five costs during the home buying process that you should be aware of.

1. Down Payment

Of course down payment is the most obvious one, so lets start there. With many loan programs, if you don’t put down a minimum of 20 percent you will be charged PMI

What is PMI?

Private Mortgage Insurance (PMI) is a mortgage insurance policy protecting the lender in case you default on the mortgage payments. Think of it like a Landlord saying your rent will be a bit higher each month because you didn’t have enough money for the security deposit.

Because of PMI, I feel it’s best to put as much money down as you can possibly afford. But as a first time home buyer, it’s highly unlikely that you can save up the 20% to get out of paying the PMI.

That’s OK, you start where you can start.

If you can start at 10 percent down, great!

5 percent, fantastic.

3 percent, that works.

If you are putting zero down, but staying inside a comfortable debt to income ratio and can start to save some extra money, that’s OK too.

Addition Resources On Private Mortgage Insurance

- What Is Private Mortgage Insurance? (PMI) | Nerd Wallet

- Private Mortgage Insurance (PMI) Is Neither "Good" Nor "Bad" | The Mortgage Reports

- How Avoiding Mortgage Insurance Helps VA Loan Homebuyers | Military VA Loan

- Can You Remove PMI From Your Mortgage? | Making Sense of Cents

Closing Costs

A cost of getting your mortgage is the closing costs, charged by lenders and third parties -- related to the purchase of the home.

Which by the way is something most buyers overlook when shopping for a lender. Buyers tend to get caught up in trying to find the lowest interest rate and completely overlook the fact that they are being charged outrageous closing costs, actually costing them more money.

Persinger Principle: Don’t look for the lowest interest rate. Shop for the mortgage trifecta, rate, closings costs and service.

Persinger Principle: Don’t look for the lowest interest rate. Shop for the mortgage trifecta, rate, closings costs and service.

Your closing costs can cost you anywhere between 2 percent - 5 percent of the total cost of the purchase.

So, in reality, if you had saved up 3 percent for a downpayment to buy a condp, you are actually only half way there.

With that being said, at Persinger Group we are pretty good at negotiating with home sellers to pay these closing costs for our buyer clients. In some cases, with a VA mortgage, the seller must pay a portion of the closing costs.

Here’s some typical things that are included with your closing costs:

- A credit report fee

- A loan origination fee, processing the loan paperwork for you.

- Discount points, a fee to buy down your interest rate even lower

- Appraisal fee, to confirm the home is valued at the correct purchase price

- Title search fees, which pay for a background check on the title to make sure there aren't things such as unpaid mortgages or tax liens on the property.

- Title insurance, protects the lender in case the title isn’t clean.

- Escrow deposit, a hold on future property taxes and private mortgage insurance, so that it’s there when needed.

- Recording fee, paid to the county, or city, to document the exchange of ownership.

- Underwriting fee, which covers the cost of evaluating a mortgage loan application.

Inspection Fees

After you get you get your offer accepted by the seller one of the first contingencies is going to be getting an inspection to make sure the condo is in good shape, safe and without any major defects. You pick out the inspector for this and it’s your cost.

And that’s a good thing.

You don’t want anyone else but you picking out the person to make sure this condo isn’t a money pit.

That cost will be anywhere between $200 - $600, depending on the size of the condo unit and inspector.

During this initial inspection, the inspector might suggest additional inspections, like a termite inspection. Any additional inspections you choose to get are also your expense.

Getting an inspection is NOT an expense you want to skip or get cheap on. When you think about the value of the condo versus the cost of the inspection, it’s entirely worth every penny. Don’t be cheap here.

A caveat to this advice is when you're in an Extreme Seller's Market. Waiving an inspection might give you a competitive advantage. We'd still suggest doing a pre-inspection. That is having the property inspected before you submit your offer, so you still know exactly what you're walking into.

Earnest Money

A couple of times I’ve thought to myself that I’m writing this guide specifically to talk about earnest money.

So many buyers are surprised by earnest money and caught off guard when we start talking to them about this during the offer process.

Earnest money is simply a way to say, “I’m serious here. And if you don’t believe me, let me put my money where my mouth is.”

Put yourself in the shoes of the seller for a second: Would you want to take your home off the market for someone that is a flake, or could flake out at any minute? Let’s pretend that you get an offer accepted on a condo and then a week later a condo in the same building comes up for sale, but it’s $10,000 less. Why not tell the seller, you’re sorry but you changed your mind and walk down the street to get a better deal?

Sounds good in theory right?

But what if the shoe is on the other foot? You get the offer accepted on a condo you love and a week later the seller comes back and says, “I’m sorry but another buyer offered me $10,000 more. I’m not selling to you any more, I’m going to sell to them.”

See, a contract is a contract, but the fear of losing money is what makes people follow the agreement and timeline. The earnest money is mutually beneficial for you and the seller.

We encourage our clients to offer a 1% of the asking price as their earnest money. And in reality, this isn’t additional costs. The earnest money, which will be held by a broker or an escrow company, will be used towards your down payment or closing costs.

So if you wrote an earnest money check for $2,500 and your lender tells you that your closing costs are going to be $5,000, you really only have to bring $2,500 now.

Moving Costs

Maybe you're not paying for a moving company but have you priced out the costs of boxes and a moving truck? Or maybe you have to take time off work for the move? And don’t forget, if you’re going to ask family or friends for help, you probably should supply some pizza and beer.

An Extra Cost To Think About

In a perfect world you could time moving into your house and when your lease ends. It’s too bad most of us don’t get to leave in this perfect world. Or maybe you can time it right, but it means missing out on the perfect property. You might want to look at your lease and figure out the costs and fees for breaking a lease early and decide if it’s worth it to you.

How many times have you broken your phone contract and paid the penalty because it was worth it for that new phone or service?

That was for a phone. This would be for your home.

It might be worth it. It might not.

But it's something for you to think about and decide.

An Extra Benefit Of Having A Mortgage

Owning a condo is great.

Painting the walls. Decorating your living room. Making the baby nursery look super cute. You get to make it yours. Your home. That’s on the emotional side of things.

On the financial side of things, you have some financial security that you know what your payment will be every month and it won’t go up at the end of the month, or six months or a year from now.

You are paying down the principal each month, so you’re increasing your equity.

Also, you’re increasing your equity in the condo by the natural appreciation value of the property.

An extra benefit of having a mortgage and being a homeowner is being able to write off some expenses like property taxes and the interest paid on the mortgage.

Compare Owning A Condo To Renting An Apartment

Let’s say Brian and Jessica just bought a home and have a $1,300 a month mortgage. About $1,000 of that includes interest. Their total yearly payments are $15,600 with $12,000 being tax deductible. Brian and Jessica are in a 25 percent tax bracket, so their tax savings are $3,000 ($12,000 x .25).

Their actual housing costs for the year are $12,600. ($15,600 - $3,000). And that doesn’t include any property tax write offs and the appreciation of the home.

Now let’s look at Jim and Kelly who don’t feel like they can afford to buy. Jim and Kelly rent a two bedroom apartment for $1,200 a month. Their housing costs are $14,400. See, even though Jim and Kelly feel like they can’t afford to buy and that they are saving money by renting and paying $100 less a month, they are actually spending $2,400 more than Brian and Jessica. Plus, they are not building any equity in debt pay down or appreciation.

Tax benefits is not the reason to buy a condo, but it’s certainly a nice extra benefit.

*Disclosure - I’m not an accountant, or a mortgage lender, or a financial planner. Talk with one of them or all of them about your specific scenario and how tax deductions can help you financially as a homeowner.

Chapter 4: How To Find Your Condo: Online Search vs Open House vs Private Tours

Start sooner than you think makes sense.

People procrastinate. I get it. That’s just what they do.

And your natural instinct will be to wait to do all the things we're sharing with you to do. You’ll want to put off talking with a lender or wait until next month to start saving money or hesitate on getting your paperwork in order.

And this creates a paradox:

The more you wait and hesitate, the more it will take later, in money, time and effort.

Buying a condo is easy, but only if you don’t start off on the wrong foot and end going in the wrong direction and getting lost wandering around there.

When Katherine and I bought our home in Lake Stevens, we had both been self-employed for a few years at that time. I was still struggling to get my consulting business off the ground and find a consistent flow of clients. Katherine was doing great in real estate sales but had just had a really down year as she was planning our wedding and got distracted by that. We knew that we wanted to buy in the next year or two, but knew it would be difficult.

Banks don’t like to lend money to self-employed people or business owners because our income is inconsistent. Each month it goes up and down. Every year it can go up and down. The underwriting process to get a mortgage is much more strenuous for self-employed people versus those that get a paycheck and a W-2. Because of this, we started sooner than would make sense for most people.

We called our lender up and invited him out to lunch. We had files of our past tax returns, bank statements and leases from the tenants of our rental properties. We told him our goals, how much house we would like to buy and our timeline of doing that in the next two years. Our lender, jotted down a page of notes as he flipped through our paperwork, asking us a few questions along the way.

Later that day, he called us and told us that we could afford something if we stayed under a certain price range and put a certain amount down. That amount wasn’t going to get us our dream home, but it was going to get us a yard for our French Bulldog, Pearl. It was also going to get us a, third bedroom and a second bathroom.

By starting sooner than you’d think makes sense, we were able to get into a home sooner. We were able to start building equity sooner and able to take advantage of appreciation sooner.

We’ve seen buyers make this one huge mistake, standing on the sidelines, waiting, afraid of their financials, fearing the process or the people involved and not getting started sooner. So when it came to us buying our next home, we were determined to not make that mistake.

And not making that mistake has paid off big for us.

Don’t make the mistake so many other buyers make. Start sooner.

“The time to have the map is before you enter the woods.”

Finding The Condo You'll Buy

OK, you’ve called the mortgage lender of your choice to get prequalified. You now have an idea of what you can afford, but don’t forget you decide what you spend.

Now that you have an idea of what you can afford, let’s get an idea of what you’re looking for.

When we sit down with a home buyer to do a “Meet & Greet” one of the questions we ask them is what are they looking for in a home.

Specifically, we ask, “What are your MUST HAVES?”

Then we ask, “What are your WOULD BE NICE?”

And finally, “What are your DEAL BREAKERS?”

With these three categories, you should start to get a good idea of what you’re looking for and “know it when you see it”, plus your real estate agent will also know it. This is important, because while you’re searching on their website, they are searching directly in the MLS and out previewing properties.

If you can communicate to them what you are looking for, there is a better chance they can find it.

According the National Association of Realtors Homebuyer Report, 33 percent of the time a real estate agent found the home a buyer purchased. Zillow research reports that just over half (51 percent) of buyers who use an agent involve them at the very beginning of their home search.

Also reported, the top service buyers want from their agents is private home tours (67 percent). They’re also depending on agents for updates on new homes on the market (58 percent) and previewing homes (44 percent). Additionally, buyers want agents to provide listings that fall outside their expressed buying criteria (31 percent).

So even though you have access to these tools and search yourself, having a Realtor that understand the market and your search criteria is still critical.

It should be noted that Persinger Group finds the property for our buyer clients 2/3’s of the time.

Why are we double the normal?

Probably because of our system, communication and ability to help our buyer clients communicate to us.

Must Haves - Three Is Enough

These are of course the things that you must have or they couldn’t pay you to move into the condo.

We think it’s a good idea to set a limitation for our clients that they can’t have more than three must haves and I encourage you to follow the same principle.

There is something freeing about forced limitations and there is a paradox of choice.

In one behavioral experiment, researchers set up inside a grocery store with table full of jam samples. In the first test they offered a huge range of 24 different jams to taste; on a different day they displayed only six. Shoppers who took part in the sampling were rewarded with a discount voucher to buy any jam of the same brand in the store.

It turned out that more shoppers stopped at the display when there were 24 jams. But when it came to buying afterwards, fully 30% of those who stopped at the six-jam table went on to purchase a jar, against merely 3% of those who were faced with the selection of 24.

It might be more fun to make a list of 24 must haves, but that makes your condo search harder, not easier.

By the way, even a genie only grants you three wishes.

WOULD BE NICE - Go Crazy

In this category, go nuts.

Just remember that when it comes time to getting serious about condo shopping, these would be nice, but are not must haves.

DEAL BREAKERS

Sometimes it’s easier to describe what you don’t want than what you do.

It’s OK to Change

Time and the search bring clarity.

Perhaps it’s while you’re still in the early stages or maybe it happens after you’ve looked at a few properties in person. You’ll start to get more clarity about what truly are must haves, would be nice and deal breakers.

None of these are in stone.

You might realize that a certain must have isn’t that critical after all and drop it from your list and move a would be nice into your top 3 must haves.

This is perfectly OK to do, just communicate it with your agent.

Where To Look For Condos Online

Not all home searches are equal. There are, what we call in the industry, third party aggregators, franchise websites and then there are websites that agents and brokers have directly connected to the local MLS.

A multiple listing service (MLS, also multiple listing system or multiple listings service) is a suite of services that enables real estate brokers to establish contractual offers of compensation (among brokers), facilitates cooperation with other broker participants, accumulates and disseminates information to enable appraisals, and is a facility for the orderly correlation and dissemination of listing information to better serve broker's clients, customers and the public. A multiple listing service's database and software is used by real estate brokers in real estate (or aircraft broker in other industries for example), representing sellers under a listing contract to widely share information about properties with other brokers who may represent potential buyers or wish to cooperate with a seller's broker in finding a buyer for the property or asset. The listing data stored in a multiple listing service's database is the proprietary information of the broker who has obtained a listing agreement with a property's seller. - via Wikipedia

Where you search for homes online matters. If you are using the wrong website you could end up frustrated and disappointed.

Use The Local Agent or Brokerage Website

By using a local agent’s or their brokerage’s website you will most likely be seeing every home that is for sale in the marketplace, including listings from every brokerage intown.

If you’re agent does not have their own website or real estate search on their website ask them why. There might be a very good reason. Maybe instead of every agent having a website, their brokerage wants their agents to redirect all clients to the brokerage website.

I can’t tell you how many times we have condo buyers searching on the PersingerGroup.com and when we connect with them, they tell us they have an agent but their agent doesn’t have a website. Without a good reason, I really feel like this is unprofessional.

Having a website with a decent search should be the minimum standard of someone who calls themselves a real estate professional. (Can you imagine calling a carpet cleaner, they show up and ask you where your vacuum and cleaning machine is?)

Why You Probably Don’t Want To Use The Websites Like Zillow To Search For Your Condo

Zillow is certainly a popular name in real estate and it feels like they are the Fandango of real estate.

But just like you probably recall from high school, just because something is popular doesn’t mean a whole lot.

Before I get accused of bashing Zillow too much, let me just say that I think Zillow is great at what they do. But in my opinion, what they do is entertain. I don’t feel like they are in the business of real estate or the place to search for condos, if you are serious about buying a condo. It's fun if you're window shopping.

In a research case study by WAV Consulting, they discovered that in the Seattle market area, for example (by the way, Seattle is where Zillow was founded and based) Zillow only shows you 72% of the homes for sale. Versus agent and brokerage websites that are directly connected to the MLS.

And while the local agent and brokerage websites show you homes instantly on the market, it can take Zillow up to 7 days to get the homes and data on their website.

And while a local agent and brokerage website will show you every home for sale, from every brokerage, 36% of the homes on Zillow aren’t even for sale.

In a recent article from Seattle Times, it founds that Seattle Zestimates are off by $40,000.

I’ve lost cost of the number of times we get an email from a buyer asking about a home they are interested in they found on Zillow, and we have to break the bad news to them that the home has already sold, or is pending, or not even for sale and sometimes it’s been two years since the property sold.

I’ve lost cost of the number of times we get an email from a buyer asking about a home they are interested in they found on Zillow, and we have to break the bad news to them that the home has already sold, or is pending, or not even for sale and sometimes it’s been two years since the property sold.

An Insider’s Look

If you’ll allow me to pull the curtain back a bit to expose the Wizard behind the curtain.

See, the business model for websites like Zillow is to simply sell advertising to real estate agents. They want inventory of homes for sale, wherever they can find it, to put on their website so they have the buyers searching on their website. Zillow then spends all day selling advertising to real estate agents. (I get multiple calls a day from businesses like this).

Then when you fill out a form on their website they give your information to a real estate agent that has paid money to get your contact information. The filtering process is not the best agent, the most knowledgeable agent, or the most competent. It’s which agent was willing to pay the fee.

Then, if you fill out another form on that website because you're interested in another property, there’s a really good chance that an entirely different agent will also get your contact information, so on, so on, repeat, repeat. Until you have multiple different real estate agents emailing, calling, texting you until you “buy or die”.

To see all homes for sale in your market area, to search for homes like a Realtor would inside the MLS, find a local agent’s or broker website.

Features Of A Website To Look For In Your Condo Home Search

- Be able to mark a property as favorite or separate homes you like from those don’t

- Location

- Map search

- Google Street-View

- Daily updates of new homes on the market and/or price reductions

- Ability to save specific searches

Chapter 5: How To Make An Offer On A Condo You Want To Buy

Something buyers will say to us often is, “I’m looking for a deal.”

Look, isn’t everyone? Who really wants to overpay for a home, a car or a Russell Wilson bobblehead doll?

But you need to understand what kind of market you're in to truly get the best deal. You can't just move forward thinking you should get 10% off. Here's why:

If you’re in an Extreme Seller’s Market and you want to get a deal, by making an offer $5,000 or $10,000 lower, don’t be surprised if the home sells for MORE than the list price. When my wife and I started looking for the Lake Stevens house, we made six offers on homes before we finally got an offer accepted.

We were shopping in an Extreme Seller’s Market and were constantly frustrated by offering $25,000 more than list price and having our offer rejected. In actuality, the list price of the home should have very little to do with the offer you make. The list price serves as an anchor and anchors aren’t always helpful.

In a research experiment of how numbers anchor decision making, visitors to the San Francisco Exploratorium were asked one of the following two questions:

- Is the height of the tallest redwood tree more or less than 1,200 feet? OR...

- Is the height of the tallest redwood tree more or less than 180 feet?

Although the answers to these two questions (less and more, respectively) were quite easy, the key question came next.

The visitors were then asked to estimate the height of the tallest redwood. People who had earlier been given the high anchor (1,200 feet) estimated an average height of 844 feet.

Those initially given the low anchor estimated that the height of the tallest redwood was 282 feet.

In each case, the (clearly incorrect) anchor played a massive role in people’s estimates. To get the best deal and not miss out on your favorite condo you need to know the market you are in, and not be attached to the anchor of the list price.

The 5 Real Estate Markets

The main way to figure out what kind of real estate market you are in is by knowing Months of Inventory and Absorption Rate.

To calculate these things you need to figure out how many homes are sold in a specific time period. Next, divide the number of homes by the number of months in the time period. Last, divide the rate into the number of current listings. This reveals the months of inventory.

The reason why this is important to know is because of Economics 101 - Supply and Demand.

The price of homes, Days on Market, etc, are all nice metrics to know but Months of Inventory is the key metric to know to when it comes to knowing the market you are in.

Example: There are 500 homes sold over a six month period.

500 / 6 = 83.3.

There are 200 homes currently for sale.

So dividing 83.3 into 200 gives you 2.4.

In this example, there are only 2.4 months of inventory.

- Extreme Seller’s Market: 0 - 2 months

- Seller’s Market: 2 - 4 months

- Balanced Market: 4 - 6 months

- Buyer’s Market: 6 - 8 months

- Extreme Buyer’s Market 8+ months

Now keep this in mind, there are multiple markets going on inside every market place. What we mean by that is, price points, neighborhoods, new construction, etc can all have different markets going on.

A price point of $200,000 - $300,000 could be an Extreme Seller’s Market, while a price point of $400,000 - $500,000 could be a Buyer’s Market in the exact same city.

By knowing what market you are in will give you great knowledge in constructing your offer. Just remember, any market can have multiple markets.

Persinger Principle: Any market can have multiple markets.

The Offer

Every state and every MLS is going to have different forms and a different process.

Allow the real estate agent to walk you through the process, contracts and don’t be afraid to ask questions.

In today’s tech filled world you can actually write an offer to buy a home without sitting down with your real estate agent. You can now “electronically sign” at home, sitting in your bed, in your underwear or at Starbucks on your phone.

Technology software like Docusign, Authentisign, and Dotloop provide a convenience to signing the paperwork. But, just because it’s convenient doesn’t mean it’s easy.

It might not be easy to figure out where to click, how to sign, what the forms mean, what you’re committing to and signing. It might be easier and you might feel more comfortable sitting down with your real estate agent to write the offer up.

Whenever a client decides to write an offer we always offer and encourage a sit down at first. If there is ever a counter offer or we have to write a second offer we make the e-signature technology available.

If you’re unsure or uncomfortable, it won’t be easy.

Don’t be afraid to let your agent know that you would rather sit down, instead of signing by yourself, electronically.

The Three Elements of an Offer On A Condo

1. Price

We already talked about price a few paragraphs back, by knowing what kind of market you are in. There are certain metrics that are nice to know also. Like, price per square foot, days on market, looking at comparables and competition.

At Persinger Group we have a proprietary 17 point metrics worksheet that we put together for our clients. Ask your real estate agent how they help you calculate the correct price to offer.

2. Terms

Believe it or not, price isn’t everything.

Maybe you care about what appliances stay. Or maybe the seller cares about the closing date. Your agent should talk to the listing agent to find out what terms are important to the seller and give them as many of the terms as you feel comfortable.

3. Contingencies

A contingency says that certain conditions must be met for the transaction to keep moving forward to closing.

The two major contingencies are financing and inspection.

Your Financing Contingency

A financing contingency basically states you will only be responsible for buying the home if you can get a mortgage.

Your Inspection Contingency

The inspection contingency lets you take a better look at the property and decide if you still like what you see. You should hire a licensed home inspector to do this. Not your buddy or cousin that, “knows a lot about homes.”

First, realize that a home inspector’s job is to find things wrong with the home. If they find something wrong, that’s good news, not bad news.

Do not be shocked, surprised or scared when you get the inspection report and the inspector finds things that are wrong with it. That would be like being upset at a bartender for making drinks. They are doing their job and they probably did it well. If they didn’t find anything wrong, honestly I would be suspicious (even for a newish condo unit).

Other Contingencies

HOA/Condo Review

Another common one will be review of the HOA or Condo Association documents. This will let you know what, if any rules or restrictions the Association has. For example, you own a boat and want to leave it parked in spot but you discover that your HOA doesn’t allow any parking of boats, trailers or recreational vehicles outside.

This also gives you an opportunity to look at their financials, which is especially important for condos.

Chapter 5.5 WAIT

“And when the day arrives I'll become the sky and I'll become the sea and the sea will come to kiss me for I am going home. Nothing can stop me now.” - Trent Reznor

Now's it's time to wait.

In the offer you can set a specific amount of time that the seller has to respond. This will likely be 24 - 48 hours. Try not to be too nervous, anxious or excited.

Counter-Offer and/or Mutual Acceptance.

There might be some back and forth with price, terms and contingencies. You might have to give on some things so you can take on others. For example, you give the sellers the closing date they want so you can get the price you want. Price isn’t everything. The type of financing you are seeking, the terms you’re asking for and the contingencies you add, all impact how “strong” the seller views your offer.

Chapter 6: It Just Got Real. Congrats!!!

You have mutual acceptance.

You and the seller have agreed to price, terms and contingencies.

It just got real, real fast. Things are going to move fast now.

The first thing you’ll want to do is let your mortgage lender know.

Second, you’re going to schedule your inspector to come take a look at the property.

Your real estate agent will get you a timeline or schedule of all the important dates.

Remember, this is a contract. The timelines matter.

If you said you would do an inspection in five days, but procrastinate on hiring an inspector and getting them scheduled, that’s a big problem.

Respect the timeline.

Condo Inspection

Remember, the inspector should have found some things wrong with the condo unit. That’s their job. Do not be shocked, surprised or scared. It’s now time to restart negotiations.

At this point, you will sit down with your real estate agent again and decide how to proceed.

We would recommend bringing back the Must Haves, Would Be Nice, & Deal Breakers priority chart.

Any of the things that your inspector listed as a problem move to this list. Anything that ends up on the Must Haves or Deal Breakers list will probably be what you ask for. If you get greedy and ask for everything that’s on the Would Be Nice list, the seller will probably feel like you are being unreasonable.

Every condo, especially single family homes, are going to have a few maintenance issues and upkeep projects. Get use to it. You’re a homeowner now.

One of the biggest challenges that I see buyers have during this phase is getting attached to a “fix.” The really want the seller to do a certain repair, so much so that they forget they could lose their condo.

A few times we’ve had buyers accuse us of not being on their side and working for them, when we suggest they are being unreasonable. We then have to ask if they think our job is to help them get a $5 rubber seal replaced or to help them get the home they want.

We stay focused on the big picture — getting the condo. Getting caught up in the smallest of things is an easy way to lose the condo you wanted.

This doesn't mean you shouldn't ask for things that matter. And possibly walking away from a property that just doesn't seem worth it any longer.

Financing

I’m surprised there hasn’t been a horror movie called The Underwriters. T

he underwriters are the nameless, faceless, perhaps soulless people who crunch numbers, and decide if you’re a wise investment.

There is a very, very, very good chance that they are going to ask for more paperwork, bank statements, letters from your work, etc, from you.

Don’t be surprised. Don’t be upset. It won’t get you any closer to getting your mortgage.

Look, if I was about to loan someone a few hundred thousand dollars I’d probably want to know as much about them as I could too. Wouldn’t you?

The appraisal will also be ordered and done during this time period. The appraisal is the way for the lender to confirm that you’re not overpaying for the home. The underwriter is going to go through all this data and give you and the lender a thumbs up or a thumbs down.

Don’t worry, if your lender has done their job upfront on the pre-approval process you should get the thumbs up and have smooth sailing. Again, this is where being organized will make things easy. Have a file or drawer where you keep all of your new bank statements and check stubs. Be prepared.

HOA/Condo Review

You’ll get a chance to discover more about the HOA, their rules, finances and what it’s like inside the community.

Here a few helpful questions to get you started on discovering some important information.

9 questions you’ll want to answers about your condo association during your review period

1. How much are the dues?

2. How often do the dues increase?

3. What’s included?

4. What are the specifics of the insurance and what insurance will you be required to carry vs. the HOA carries it for you?

5. Financials – look at the last few years of statements as well as the most current and the approved future budget.

6. Are there reserves?

7. Any special assessments coming up?

(A special assessment is a one time fee to pay for something. You want to find out if there is the possibility of FUTURE assessments, if there are any currently, and if there ever HAVE been any.)

8. Find out the current status of all the membership dues. How many people are not paying or past due? How much?

(Get the minutes from the past years HOA meetings and read through to see what they talk about and this will tell you how picky they are and what type of violations they pursue action on.)

9. Any restrictions or rules that would impact what you want?

Let’s say you have your heart set on painting your front door red. Can you do that? You want a BBQ grill on your balcony. Are you allowed? What is guest parking like?

Chapter 7: What To Expect As You Get Ready To Close On Your Condo

It’s weird that it’s called a closing even though this is the final event that takes place to allow you to get the keys and open your door and start this new chapter of your life.

It’s weird that it’s called a closing even though this is the final event that takes place to allow you to get the keys and open your door and start this new chapter of your life.

We wish it was called the opening.

The closing process varies greatly from state to state. Having sold real estate in two different states, Wisconsin and Washington, and having worked with brokerage clients in various states and even in Canada, I can confidently tell you there is no one size fits all from state to state.

For example, in Wisconsin the buyers and sellers would come in and sit down at a table together, sign all the paperwork at the same time and the seller would turn the key over to the buyers.

In Washington, the title and escrow company can send a notary out to where the seller or buyer are and they typically sign before the actual closing date.

This is where being a control freak will not suit you.

It’s impossible to know at the time you write the offer exactly when and where you’ll be signing. But as you get closer to the closing date things will start to become more clear.

Your mortgage lender will be in contact with you and let you know how much money you need to bring to the closing.

Your real estate agent will be in communication with you with any updates, what to do next and who you need to be talking with.

The escrow/title company, depending on how it’s done in your state, will also start communicating and coordinating with you.

There will be a lot of moving parts and it might feel stressful or even chaotic, but it’s like a crescendo in a music piece.

Everything is just getting more exciting because it’s getting closer to your Move In Day.

Chapter 8: Frequently Asked Questions About Buying A Condo (& Questions You Should Ask)

Question: How do I understand condo fees and how do I know if they're justified or not?

Answer: Realistically, you probably won't fully understand the condo fees on a specific development until you see and review the CC&R's, disclosures and the budget. Each condo development will have different offerings and different fees.

A thing to remember is that the condo association is not for profit. Owners aren't being charged EXTRA money to line the pockets of someone. Your monthly condo dues is actually still your money. It's not only be used for common area upkeep but future expenses also.

Question: What is a special assessment?

Answer: If a condo association runs into a situation where funds are falling short and/or a project needs to be done sooner, rather than later, and the association needs money quickly they will issue a special assessment.

Question: Do condos make good real estate investments?

Answer: Depends. First if the numbers make sense, it's always a good investment. Second, not all condos allow there to be rentals. And most have what is called a rental cap. Meaning only a percentage of condos are allowed to be rented. So if you find a condo where your mortgage, taxes, fees, etc are less than what you will get in rent, AND you are allowed to rent out your condo unit... Yes. Condos make great real estate investments.

Questions To Ask When Finding Your Realtor:

- How many transactions have you been involved in?

- Do you work in real estate full time? W

- hat percentage of your business is working with buyers?

- How familiar are you with the area where I want to purchase?

- Do you have references/reviews from other buyers who have used your services?

- Can you help me with the loan process?

- Do you have a list of lenders, home inspectors, insurance agents, and other professionals to recommend?

- How do you get paid?

- Do you have a written agreement I have to sign?

- What are the terms of that agreement?

- Does it cost me anything?

- Do you have a home search website you recommend?

- What if I see a for-sale-by-owner house on my own?

Questions To Ask When Finding Your Mortgage Lender:

- What is the par rate (the actual rate for a particular loan) for a 30-year fixed loan?

- Can you estimate and explain your fees?

- Are you going to hold this loan or sell it?

- What is the interest rate you are offering, and how did you arrive at it?

- How do I know this is the best rate?

- How will the rate change over the life of the loan?

- If an adjustable-rate mortgage (ARM), what is the worst-case scenario I could face when the rate resets?

- Are you locking in my rate? For how long? What does the lock cost me?

- Could you estimate closing costs for my loan?

- Can you explain an APR, and what is it for this loan?

- What am I paying in points?

- Do I need to pay private mortgage insurance (PMI?)

- Are there any prepayment penalties on this loan?

- How often do you miss the original closing date of a mutual agreement?

- Can I talk with a few of your last transactions (agent or buyer) and ask them about working with you?

Questions To Ask When Finding Your Home Inspector:

- Are you licensed? Bonded?

- Do you have "Errors and Omissions”?

- Can I be present at the inspection?

- What does the inspection include and what does it leave out?

- Could you send me a sample inspection report?

- How many inspection have you done?

- How long will it take?

- How much will it cost? If I don’t buy this condo, how much would you charge for another inspection?

READY TO BUY A CONDO? WHAT'S NEXT?

You can start your search here if you're looking for a condo in King County. Or here if you're looking for a condo in Snohomish County.

If you have questions about buying a condo in our area or anywhere, you can email us.